Financial planning involves working with a professional to navigate through the complexities of investment, taxation and changing rules and regulations. By working together you can navigate a pathway to reach your specific goals, preferences and aspirations.

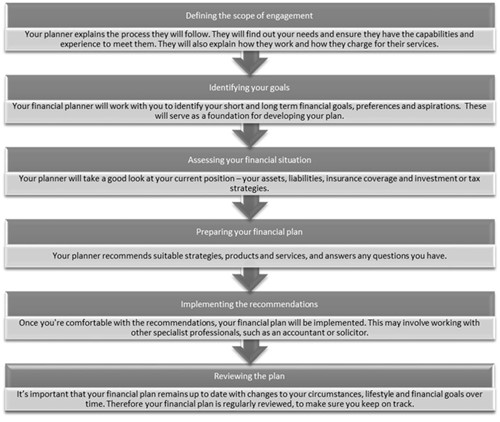

Financial planning can help you through all stages of your life. The financial planning process involves the following six steps:

To gain the most value out of the financial planning process there are three fundamental issues that are important for you to consider and understand. These key components are discussed below.

The starting point for any plan is to set your personal goals. Financial goals are likely to be different for each person and need to reflect your specific preferences, aspirations and needs. Your goals may vary from short-term goals (less than one year) like buying a car, paying off your debt or going on a holiday, medium term goals (1-3 years) such as saving for your children’s’ education or long-term goals (5 years or more) like saving for a comfortable retirement and leaving behind a legacy.

Your goals will be more real and achievable if you can apply the following attributes:

Once you have determined where you are heading, you can work with your financial planner to develop the pathway to achieving your goals.

To put you on the path to building your wealth you need to start saving money. This may mean working out how to find more money. The best way to do this is to set yourself a budget.

Setting a budget is important for everyone no matter your age or how much money you have. It is especially important for people who are struggling to meet their goals or who keep building up debt.

A budget is not about just cutting expenses. It is about finding a good balance between your income and your expenses and deciding what is important to you so that you have money left over to save. A budget is not a fixed forever plan. You can continue to make adjustments over time until you reach a comfortable outcome and have a good strategy in place that will meet your goals.

There are two sides to a budget: